We live in an increasingly digital and highly transactional world, where financial literacy can be a life-changing skill. Yet, money management is still not a formal part of the school curriculum in India. Teach kids about money early as it helps them grow into financially responsible adults.

It builds their decision-making skills, cultivates discipline, and reduces the likelihood of debt traps later in life. The earlier kids learn the basics of earning, saving, spending, and investing, the better equipped they’ll be for a secure financial future.

Why Financial Education for Kids Matters?

A 2023 survey by the National Centre for Financial Education (NCFE) found that only 27% of Indian adults are financially literate. That means more than two-thirds of the population lacks basic financial knowledge, something that could have been avoided with early exposure to money concepts. In a time when digital payments, online shopping, and credit cards are becoming the norm, children must be prepared to navigate financial choices wisely from a young age.

1. Start with the Basics: Earning, Saving, Spending

Children as young as 5 can grasp simple concepts like what money is and why we use it. Use play money, board games like Monopoly or The Game of Life, or even role-playing scenarios like a pretend shop to introduce these ideas.

- Earning: Talk about how people earn money through jobs and effort.

- Saving: Introduce the idea of saving a portion of money for future needs.

- Spending: Teach how money is used to buy things and why choices matter.

Set up a transparent piggy bank or jar system labeled “Spend,” “Save,” and “Share” to make it tangible.

2. Involve Them in Household Budgeting

One of the smartest and most practical ways to teach kids about money is by involving them in household financial decisions. Let your children see how budgeting works for groceries, school supplies, or monthly electricity bills.

- Take them shopping and show how you compare prices.

- Involve them in planning a monthly grocery budget.

- Let them make choices within a set budget—say ₹200 for a weekly treat.

This not only teaches budgeting but also instills value for money and delayed gratification.

3. Open a Minor Bank Account

Most Indian banks allow parents to open joint savings accounts for minors. This can be a powerful tool to teach children about banking, interest, and the importance of saving.

Encourage your child to deposit birthday money, cash gifts, or even a part of their allowance. Periodically check the balance together to track how savings grow.

Some banks also offer educational tools with these accounts to gamify saving and budgeting. For example, SBI and HDFC Bank have child-focused savings plans with growth calculators and visual dashboards.

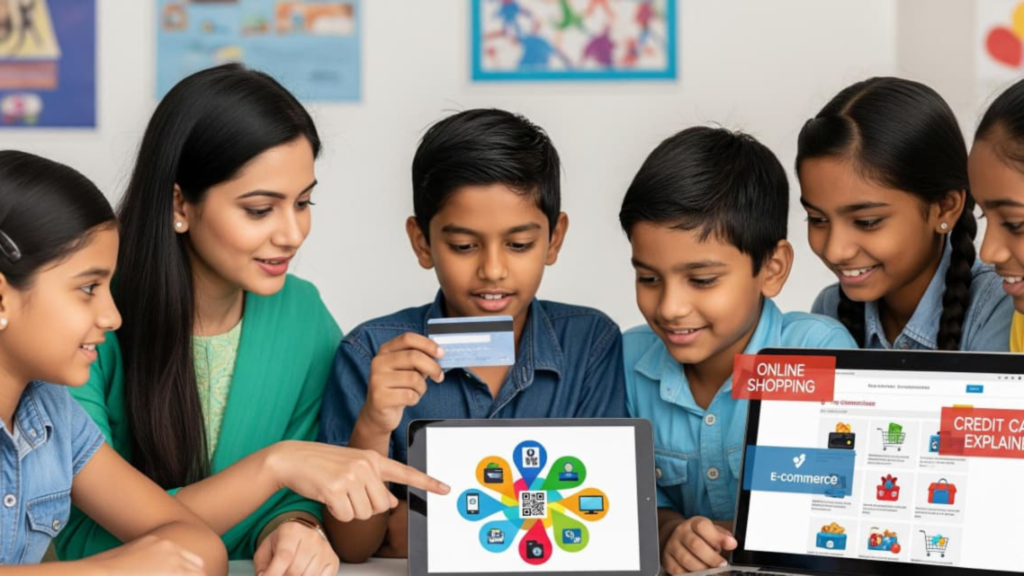

4. Use Digital Tools Wisely

With India leading the world in digital payments, children must understand how money works in the online space. According to a 2024 report by RBI, over 88 billion UPI transactions were recorded in India last year—a clear sign of how money is evolving.

- Introduce prepaid cards or digital wallets with parental controls (like Fyp or Junio).

- Teach them about transaction safety, OTPs, and the dangers of phishing.

- Set boundaries on online purchases, gaming subscriptions, or in-app buys.

Teaching responsible digital spending is as important as traditional financial education today.

5. Teach Goal-Based Saving

Kids often want toys, gadgets, or bikes. Instead of handing these over, use these desires to teach them how to save toward a goal.

For instance:

- Your child wants a cricket bat worth ₹2,000.

- You agree to match any savings they contribute.

- Set weekly savings targets and track progress visually on a chart.

This teaches delayed gratification, planning, and prioritization.

6. Introduce the Concept of Investing

While it might seem early, older kids (10–15 years) can understand basic investment ideas like how money grows over time.

- Explain interest through examples (e.g., fixed deposits or PPF).

- Use stories or simple animations about stocks and mutual funds.

- Talk about how SIPs work using examples like planting a tree that grows over time.

Apps like Piggy Ride or EduFund offer kid-friendly finance courses and investment education in a fun and engaging way.

7. Encourage Earning Opportunities

Teenagers can be encouraged to earn through small tasks, creative projects, or internships.

- Paid chores beyond regular responsibilities.

- Starting a craft or tutoring business.

- Freelancing simple tech or design work (for teens aged 15+ with supervision).

This not only builds confidence but also teaches the value of hard-earned money.

8. Lead by Example

Children learn best by observing adults. If parents are financially disciplined, talk openly about savings goals, and avoid impulsive spending, kids will naturally follow.

- Set family saving goals, like a vacation or a new gadget, and track progress together.

- Avoid unhealthy money talk, like constant complaining or stress around finances.

Final Thoughts

India is changing rapidly, and so is its financial system. By teaching children, the value of money early, we empower them to make informed choices, avoid debt, and build a secure future. It’s not about making them experts in taxation or mutual funds, but about laying a foundation of awareness and discipline that grows with them.

As Warren Buffett rightly said, “The more you learn, the more you earn.” Let’s give India’s next generation the financial head start they deserve.

FAQs

1. At what age should I start teaching my child about money?

You can begin as early as age 5 with basic concepts like saving and spending.

2. Are there any financial literacy programs for kids in India?

Yes, platforms like EduFund, Fyp, and NCFE’s FLAP offer age-appropriate content for kids.

3. Is it safe to give digital wallets to children?

With parental controls and supervision, kid-friendly wallets like Junio or Fyp are safe tools to teach digital spending.