Understanding credit scores is very important for your financial well-being, but still, credit score myths persist, leading to confusion. Here’s a clear, fact-based breakdown of common misconceptions paired with recent Indian statistics to help you separate myth from reality.

Credit Score Myths You Must Ignore

1. “Checking your own credit score lowers it.”

The truth: Checking your own credit score generates a soft inquiry and does not affect your score. In fact, routinely monitoring it helps detect errors and spot fraud early.

2. “Higher income equals a better credit score.”

The truth: Income is not a factor in credit score calculation. Your repayment consistency, credit utilization, and history matter, not how much you earn.

3. “Closing a credit card erases past debt history.”

The truth: Closing a card does not remove its history. Repayment behavior—good or bad—remains on your report for years. Lenders can still see past mistakes or successes.

4. “Never borrowing guarantees a perfect score.”

The truth: No credit activity often leads to no score. Without a history, lenders can’t assess your creditworthiness, making loan approvals more difficult.

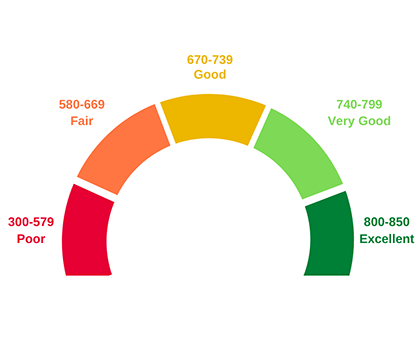

5. “All credit bureaus and credit scores are the same.”

The truth: India has four RBI-licensed credit bureaus—CIBIL, Experian, CRIF High Mark, Equifax—each using different scoring models. Scores may vary across bureaus.

The image above shows the Equifax credit score range chart.

6. “A bad credit score lasts forever.”

Reality: Poor scores can improve with disciplined financial behavior. Settlements or defaults remain on your file, but consistent EMI payments and low utilization can rebuild your score over 3-6 months.

7. “Debit cards help build your credit score.”

Reality: Debit cards don’t influence your credit score as they’re not part of credit reporting. Only credit products like loans or credit cards affect your score.

8. “Checking your credit report exposes it to unauthorized parties.”

Reality: Your credit report is confidential. Only entities you authorize (like banks during loan applications) can access it. Lenders must obtain your consent before a hard inquiry.

9. “Closing old accounts increases my score.”

Reality: On the contrary, closing old accounts can shorten your credit history, unexpectedly reducing your score since credit tenure accounts for around 15 % of your score.

10. “Having settled a loan is the same as timely repayment.”

Reality: A settled account indicates you missed payments originally. Its negative history remains on your credit file and may lower your score.

Also Read:

- Smart Ways to Teach Kids About Money Early

- Financial Planning and 10 Practical steps to Do It Effectively

Latest Insights to Think Upon

- Women are excelling in credit health. A 2023 TransUnion CIBIL report shows 57 % of women borrowers have prime credit scores (731-770 and above), compared to 51 % of men. Additionally, women have a lower 90+ days past-due delinquency rate (5.2 % vs. 6.9 %).

- Credit health varies across regions. According to the Paisabazaar “How India Checked Credit Score” report (Aug 2025), Delhi leads with an average credit score of 746, and 46 % of its residents maintain healthy credit. Cities like Pune, Kerala, and Chandigarh also demonstrate strong creditworthiness.

Summary Table for Credit Score Myths

| Myth | Reality |

| Checking score lowers it | Soft checks don’t affect your score |

| High income = high score | Score based on behavior, not income |

| Closing card erases history | History remains, positive or negative |

| Never borrowing is good | No history means you have no score |

| All bureaus are same | Different bureaus, different scores |

| Bad score lasts forever | Score can improve with discipline |

| Debit cards build credit | Only credit products matter |

| Credit report is public | Only authorized access allowed |

| Closing old accounts helps | Long history is beneficial |

| Settling = good repayment | Settlement still carries negative mark |

Tips to Build and Maintain a Strong Credit Score

To dispel myths and take actionable steps, follow these habits:

- Check your score regularly from major bureaus to catch errors early.

- Pay EMIs and credit card bills on time.

- Maintain credit utilization under 30%, ideally under 25%.

- Avoid multiple loan/card applications in a short span.

- Retain older credit accounts unless they are unnecessary or expensive.

- Dispute inaccuracies promptly.

- Use secured/low-limit cards or small personal loans to build history if you’re credit-thin.

Conclusion

Credit scores may seem complex, but many beliefs surrounding them are myths, especially in the Indian context. Armed with a little knowledge and recent data, you can confidently manage your credit.

Remember: The score doesn’t define you; your financial behavior does. Keep learning, stay vigilant, and build credit with intention.