If you are trying to learn how to master personal budgeting, it is easy to get overwhelmed by complex spreadsheets and tracking every single transaction. For many, rigid financial plans lead to burnout. That is where the 50/30/20 budget rule comes in.

Originally popularized by financial experts, this approach simplifies your personal cash flow management by dividing your after-tax income into three broad, manageable buckets. Here is a practical breakdown of the 50/30/20 budget rule explained in detail, along with how to implement it to reach your long-term goals.

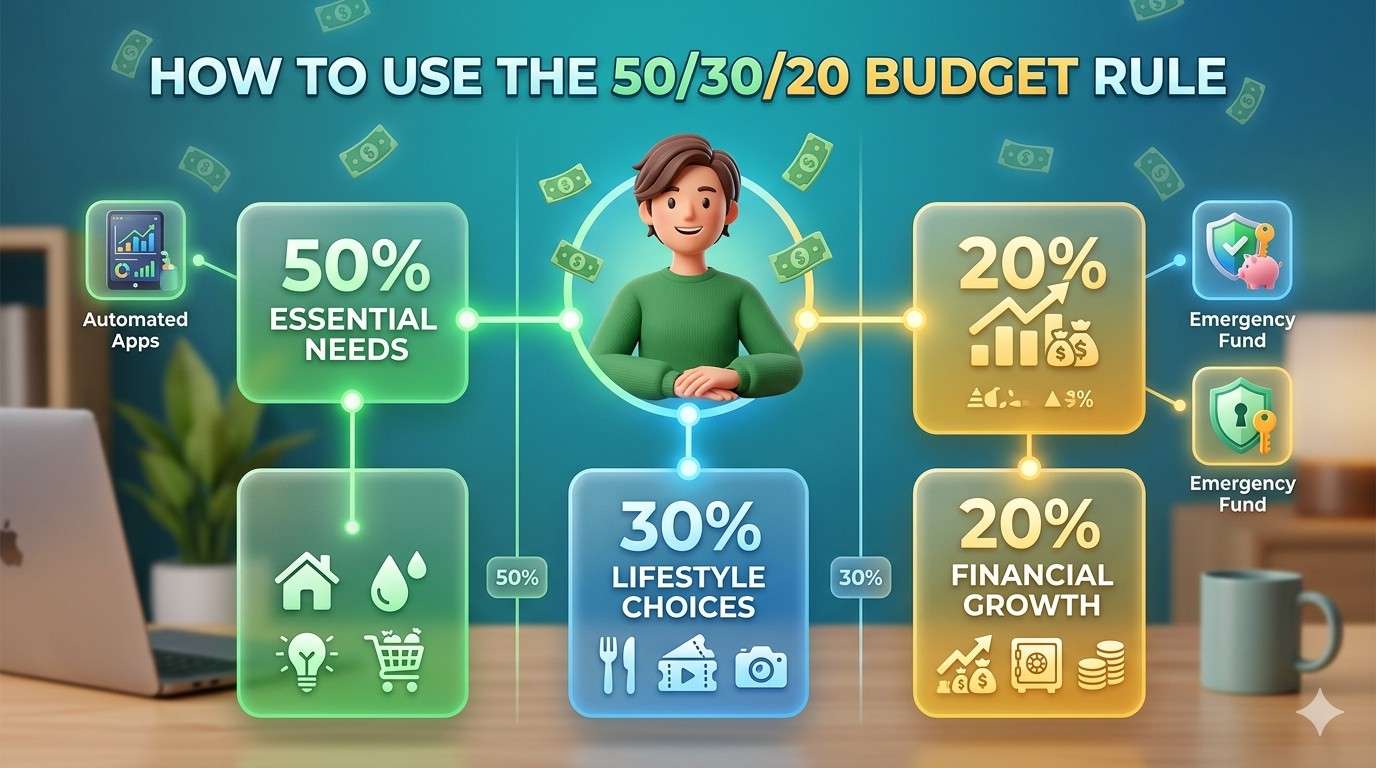

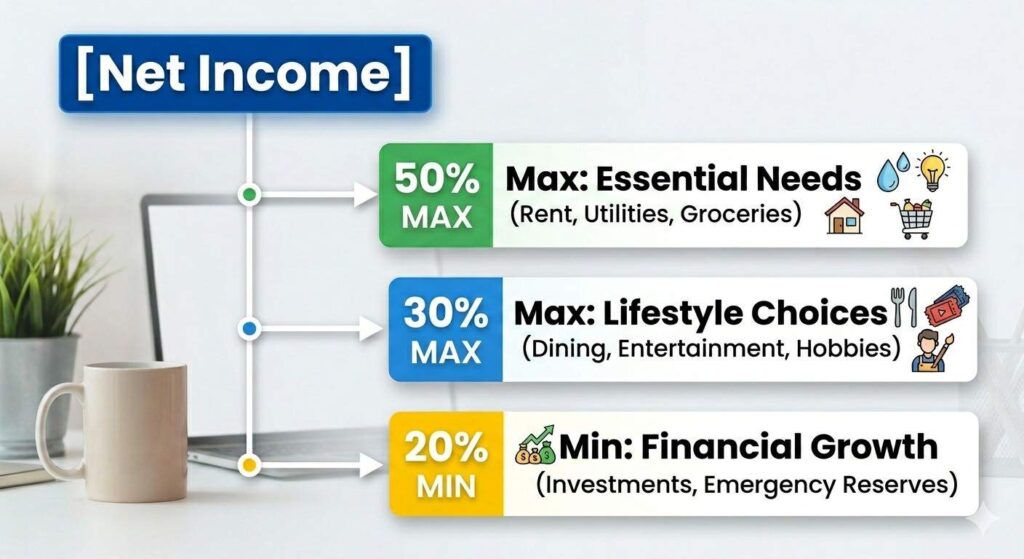

What is the 50/30/20 Budget Rule?

The 50/30/20 system is one of the most reliable financial allocation frameworks because it balances your current lifestyle needs with future wealth creation. Instead of restricting your spending completely, it creates upper limits for consumption and lower limits for saving.

The system breaks your net income down into three distinct operational pools:

1. 50% for Essential Needs

The first half of your income goes toward non-negotiable living expenses. These are the bills you must pay to keep a roof over your head and maintain basic functionality.

- Examples: Rent or mortgage payments, utilities, basic groceries, insurance premiums, transportation, and minimum required debt payments.

2. 30% for Lifestyle Choices (Wants)

This category represents your discretionary spending. It covers choices that enhance your quality of life but are not strictly required for survival.

- Examples: Dining out, coffee runs, streaming subscriptions, hobbies, travel, and entertainment.

3. 20% for Financial Growth Engines

The final portion is reserved strictly for securing your future. This is the engine room of your long-term wealth preservation.

- Examples: Contributions to retirement accounts, investments in index funds, extra principal payments toward high-interest debt, and building an emergency fund.

Step-by-Step: How to Split Your Monthly Income

Ready to put this into practice? Follow these four steps to implement this structural framework into your routine:

Step 1: Calculate Your Net Take-Home Pay

Do not use your gross salary for this calculation. Look at the exact amount deposited into your bank account after payroll taxes, insurance deductions, and automatic retirement contributions have been taken out.

Step 2: Categorize Your Last 90 Days of Expenses

Review your recent bank statements. Sort your recurring transactions into needs, wants, and savings. Be completely honest with yourself—high-end organic groceries or premium gym memberships often straddle the line between a need and a want.

Step 3: Align Your Spending with the Ratios

Multiply your net monthly income by 0.50, 0.30, and 0.20 to find your exact spending caps. If your current spending on needs exceeds 50%, you will need to look for ways to reduce fixed overheads (like downsizing or shopping for better insurance rates) or temporarily scale back your lifestyle wants.

Step 4: Automate the Allocations

The easiest way to ensure consistency is to remove human friction. Set up automatic transfers so that the moment your paycheck hits your account, 20% is instantly moved to your savings and investment vehicles.

Moving Beyond the Basics

While this framework provides an excellent balanced baseline, maintaining structural control requires the right tools and safety nets.

As your cash flow starts running smoothly, tracking your category limits becomes much easier when you utilize digital tools. To streamline this process without manual entry, read our comprehensive review of the best automated budgeting apps to find a platform that automatically organizes your transactions into these exact buckets.

Furthermore, remember that your 20% savings bucket has an immediate priority before you begin aggressive market investing. You must protect your budget from unexpected life crises. You can systematically build this defensive buffer by following our [step-by-step guide to building a 6-month emergency fund].

By executing the 50/30/20 rule consistently, you will find that how to master personal budgeting isn’t about restriction—it’s about creating a repeatable system that gives you total control over your financial independence.