Money gives us choices, but without a concrete plan, those choices quickly evaporate. Millions of professionals work demanding hours only to ask themselves the exact same frustrating question at the end of every month: Where did it all go?

The problem isn’t a lack of income; it’s a lack of structural control over your cash flow. If you want to stop living paycheck to paycheck, you must learn how to master personal budgeting through intentional asset allocation.

True financial freedom isn’t about depriving yourself of daily joys. It is about taking command of your personal cash flow management so that every single unit of currency you earn is deliberately directed toward building the life you actually want.

This comprehensive guide transforms money management from a restrictive chore into a strategic blueprint for wealth. Whether your objective is to wipe out consumer debt, purchase a home, or scale an independent consulting practice, understanding how to master personal budgeting is the non-negotiable first step to long-term stability.

1. The Psychology of Wealth vs. The Illusion of Consumption

Before opening a spreadsheet or downloading a software tool, you must understand why traditional financial tracking feels so painful. For many people, a budget is like a financial diet where they restrict their spending to a certain limit or certain categories without proper planning.

A highly restrictive financial allocation frameworks almost always fail because they focus entirely on what you cannot spend.

To successfully implement strategic budgeting methods, you must shift your mindset from deprivation to empowerment. A budget doesn’t tell you what you can’t do; it tells your money exactly what it must do.

The Hedonic Treadmill

As income increases, lifestyle expectations and desires rise in tandem. This phenomenon explains why individuals making excellent salaries can still live paycheck to paycheck. Without learning how to master personal budgeting, your spending naturally expands to consume your entire income.

Opportunity Cost Awareness

Every impulsive purchase carries an invisible price tag: the future value of that money if it had been invested. By actively tracking your cash flow, you stop looking at purchases in isolation and start evaluating them against your long-term life objectives.

2. Setting Your Financial North Star: Short, Medium, and Long-Term Goals

A budget without clear goals is like a ship navigating without a compass; you will drift aimlessly until a financial storm hits. If you want to know how to master personal budgeting efficiently, your monthly cash flow must actively fund three distinct horizons:

- Short-Term Goals (0–1 Year): Building an immediate safety net, wiping out high-interest credit card debt, and saving for predictable, non-monthly expenses like annual insurance premiums.

- Medium-Term Goals (1–5 Years): Accumulating a down payment for property, securing capital to launch an independent venture, or funding higher education.

- Long-Term Goals (5+ Years): Investing consistently in index funds, building cross-generational wealth, and achieving complete retirement independence.

Quantify these goals with hard numbers and deadlines. Knowing that you need a specific amount for a business launch fund in 18 months makes it vastly easier to pass on unnecessary everyday luxuries.

Related article – Creating a Realistic Financial Budget for Effective Financial Planning (With Example)

3. The Core Frameworks: Choosing Your Allocation Architecture

There is no single “correct” way to track your money. The best framework is the one you can stick to consistently for years. As you discover how to master personal budgeting, consider these three effective, battle-tested budgeting architectures:

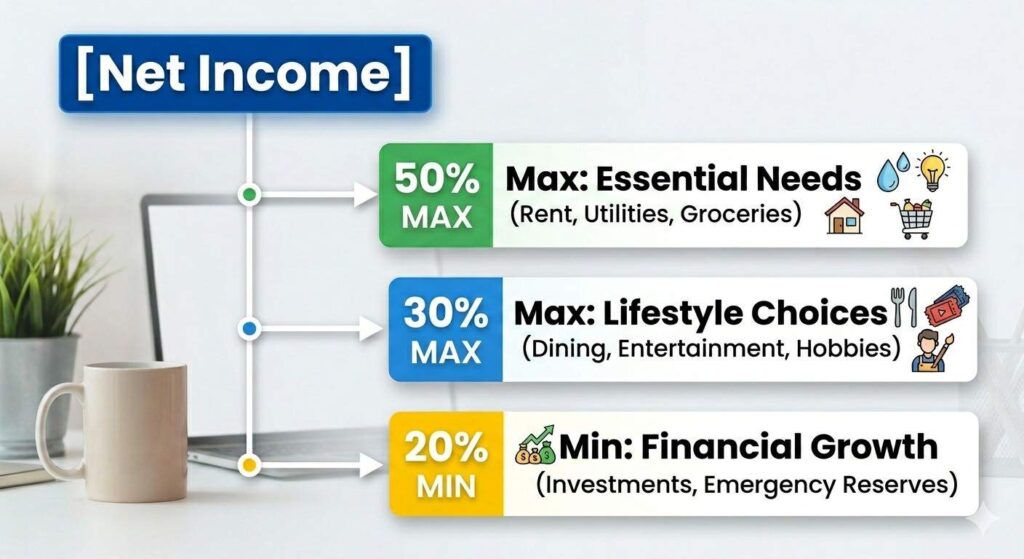

Framework A: The 50/30/20 Rule (The Balanced Baseline)

This framework divides your post-tax income into three distinct buckets:

- 50% for fixed essential needs

- 30% for variable lifestyle choices, and

- 20% for savings and debt reduction.

This framework balances structural flexibility with a guaranteed baseline for wealth building. For a complete tactical breakdown of how to segment your monthly income using this methodology, read our comprehensive guide on the 50/30/20 budget rule explained in deep detail.

Framework B: Zero-Based Budgeting (The High-Precision Model)

The mantra here is simple: Income minus Expenses equals Zero. At the start of the month, every single dollar of income is assigned a specific job. If you have any money left over at the end of your planning session, you must allocate it somewhere, which forces absolute awareness and eliminates passive leaks.

Framework C: Pay Yourself First (The Reverse Budget)

If tracking every transaction feels exhausting, this is your solution. The moment your paycheck hits your account, you immediately route a fixed percentage directly to your investments and savings accounts. Whatever remains in your main account is yours to spend completely guilt-free.

4. The Step-by-Step Execution Plan

To move from theory to bulletproof execution, follow this systematic four-step implementation process to solidify your financial baseline.

Step 1: Calculate True Net Income

Do not base your plan on your gross salary. Look strictly at your net take-home pay—the exact amount deposited into your account after taxes and deductions. If you run a business or have fluctuating freelance revenue, calculate your average net income over the past six trailing months and use a conservative baseline.

Step 2: Audit Historical Spend

Pull your bank statements and credit card bills from the last 90 days. Group every transaction into its true category. Be brutally honest here; look closely at forgotten streaming subscriptions, recurring software tools you rarely open, and the true cost of convenience apps.

Step 3: Establish Structural Caps

Using your chosen framework, establish firm upper limits for your spending categories.

Step 4: Review and Adjust Bi-Weekly

A budget is a living document, not a stone tablet. Review your actual spending against your caps every two weeks. If you overspent on dining out in week two, adjust your entertainment allocation downward for the remaining weeks to keep your month-long totals balanced. Knowing how to master personal budgeting requires this type of active, regular optimization.

5. Tracking Expenses with Technology

The mechanics of tracking your spending shouldn’t get in the way of your financial consistency. Choose a tracking medium that aligns perfectly with your personal habits and tech preferences.

The Automated Fintech Ecosystem

For the modern professional, manual entry is often a fast track to abandonment. Utilizing automated apps allows you to securely link your financial accounts for real-time tracking. These platforms automatically pull transactions, categorize your spending via algorithms, and send immediate alerts when you approach your category limits. To choose the right platform for your accounts, explore our hands-on review of the best automated budgeting apps.

Manual Ledger Tracking

For those who prefer granular control, a dedicated spreadsheet or physical ledger is unmatched. It forces you to look at every single transaction, fostering a deeper psychological connection to your cash flow and reinforcing your daily awareness of how to master personal budgeting.

6. Building the Emergency Funds

The absolute fastest way to destroy a well-planned financial strategy is an unexpected crisis. Without a financial buffer, a sudden medical emergency, a major mechanical breakdown, or a sudden client loss will force you to rely on high-interest credit lines. This derails your goals and pulls you backward into a cycle of debt.

The Golden Rule of Financial Stability: You must decouple your daily budget from unexpected life emergencies.

Before ramping up aggressive long-term market investments, your primary operational goal must be constructing a liquid safety net. You can implement this defense systematically by following our [step-by-step guide to building a 6-month emergency fund]. This fund should sit in a completely separate savings account where it remains entirely disconnected from your daily debit card or transaction avenues, acting as an insurance policy designed to buy you time and peace of mind.

Also read: What Is an Emergency Fund and Why It’s a Financial Lifesaver

7. Overcoming Common Obstacles and Budget Leaks

Even the most meticulous financial plans run into friction. Here is how to handle common threats to your progress as you learn how to master personal budgeting:

- Irregular Expenses (The “Sinking Fund” Fix): Annual software renewals, holiday gift-giving, and vehicle maintenance aren’t surprises—they are predictable, non-monthly costs. Calculate the annual total for these expenses, divide by 12, and set that amount aside inside a dedicated monthly “sinking fund” so the money is waiting when the bill arrives.

- Lifestyle Creep: When you hit a major milestone—like a salary increase or a highly profitable client contract—immediately route at least half of that new income into automated investments. This allows you to celebrate your success by enjoying a small lifestyle upgrade while ensuring your wealth engine scales even faster.

- The All-or-Nothing Trap: Slipping up and overspending on a weekend trip does not mean your framework failed. Don’t throw away the entire month’s plan. Acknowledge the extra spend, recalibrate your targets for the remaining weeks, and continue moving forward.

Learning how to master personal budgeting is ultimately less about complex math and far more about behavioral consistency. By taking deliberate control of your cash flow, deploying structural allocation models, leveraging modern automated tracking tools, and securing your progress with a dedicated financial buffer, you move decisively out of defensive survival mode. You build a repeatable, scalable financial system that turns your hard-earned income into lasting independence.